Middle East Producers Eager To Hike Prices As Russian Oil Ban Looms

Chinese COVID-19 lockdowns will be a much bigger threat to regional demand in Asia than initially assumed.

Looming EU-ban on Russian crude may further improve demand for Middle East crude grades.

Middle East producers continue to hike prices, but not as aggressively as anticipated.

The volatility that we have seen in the oil markets over March will most certainly become part of history books. In the same month that saw OPEC production decline for the first time in more than a year (primarily because of Iraq), the idea of banning Russian crude became a wholly realistic scenario, spearheaded by the US going for a full-blown sanctions package. What might have set the stage for the steepest monthly increase in outright prices was eventually cooled down China going down with coronavirus lockdowns which started off as a largely innocuous manifestation of the country’s zero-COVID policy but have gradually shed almost 1 million b/d off China’s total crude demand. All this has seen Middle Eastern producers set formula prices for May 2022 and combining weaker demand with lower physical crude availability, albeit partially offset by the US SPR release, turned out to be a much harder challenge than one could assume. Chart 1. Saudi Aramco’s Official Selling Prices for Asian Cargoes (vs Oman/Dubai average).

Having withstood the pressure coming from major importers to increase the OPEC+ monthly additions, Saudi Aramco increased all its May-loading formula prices for the second time in a row. The Asian price increases were particularly interesting. With the Dubai cash-futures (the M1-M3 spread) rising by almost $5 per barrel in March, the market anticipated huge month-on-month hikes and Saudi Aramco delivered. Consequently, the Asia-bound May OSPs of Arab Light, Arab Medium and Arab Heavy all saw increases of $4.40 per barrel each, taking the former two to premiums above $9 per barrel vs the Oman/Dubai average. This means that the Asian formula prices of every single grade was hiked to an all-time high, even higher than in the last months before the pandemic. It should be noted that March was relatively weak in terms of overall Saudi exports, the overall flow decreased by 400,000 b/d according to Kpler data, at the same time exports to Asia remained stable so there seems to be a manifest preference to keep Saudi Arabia’s regional clout in Asia intact.

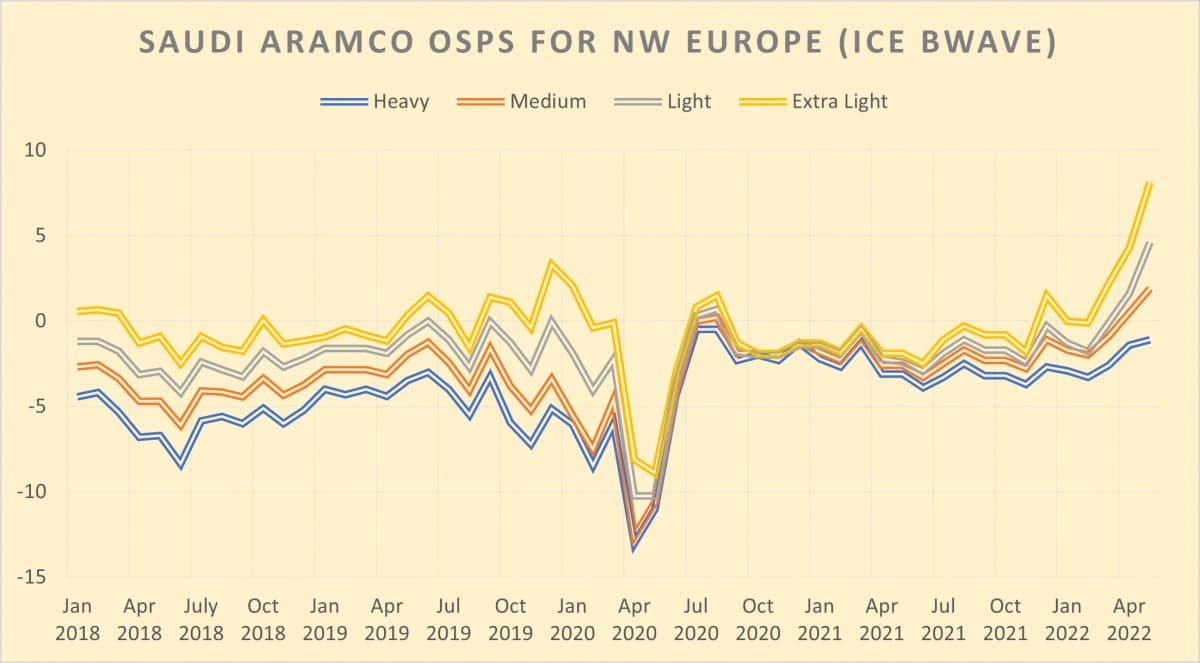

Chart 2. Saudi Aramco’s Official Selling Prices for European Cargoes (vs ICE Bwave).

For European buyers Saudi Aramco went for price increases of $0.60-$3.80 per barrel, with the highest hikes reserved for the lightest grade. At the same time, the May OSP of Arab Medium to both NW European and Mediterranean buyers was raised by ‘only’ $1.40 per barrel, arguably because the grade is the closest to Urals that the market has to offer. When it comes to the United States, it might seem that Saudi Aramco is aware that outbound flows to the USGC will be minimal in the foreseeable future. The Saudi NOC hiked all its US-bound cargoes by $2.20 per barrel, as a result of which even the heaviest and sourest Arab Heavy will wield a $4.5 per barrel premium vs ASCI in May (for reference, the Basrah Heavy-Arab Heavy will stand at a whopping $7 per barrel, unprecedentedly wide). Bluntly put, Saudi Aramco has placed the least priority on maintaining US exports, already at a low point of 200,000 b/d recently.

Chart 3. ADNOC Official Selling Prices for May 2022 (set outright, here vs Oman/Dubai average).

Whilst ADNOC’s April pricing might retrospectively seem a great gift to the usual buyers – Murban was fixed at $93.99 per barrel in a period of triple-digit prices – the official selling price of May-loading cargoes inevitably edged up by almost $20 per barrel, to $112.48 per barrel. Whilst there has been little talk of ADNOC overall, the United Arab Emirates arguably saw the most linear upward progression over the past months. With gradually increasing production, up went UAE exports, too, marking a series of consecutive month-on-month hikes since November 2021. Total exports in March have averaged just below 2.8 million b/d, some 700,000 b/d higher year-on-year. With ADNOC already stating that it would supply full June nominations, the stage is set for a continuation of the same step-by-step production increases.

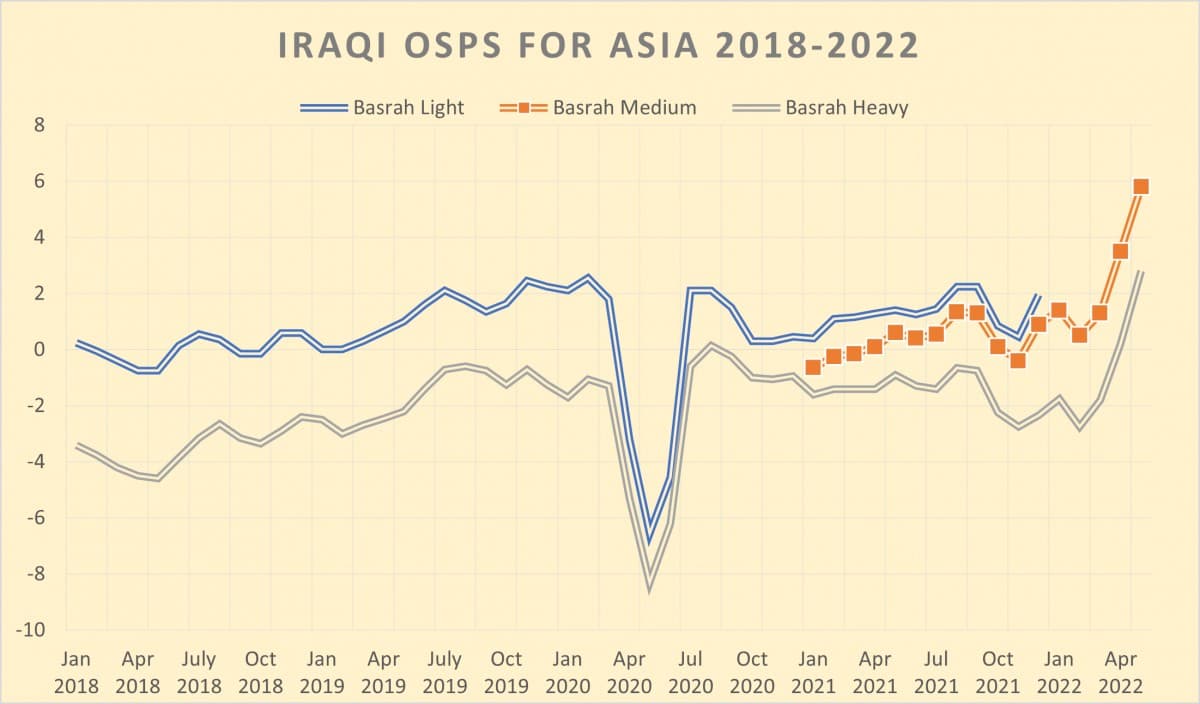

Chart 4. Iraqi Official Selling Prices for Asian cargoes (vs Oman/Dubai average).

The real pricing policy surprise came from the Iraqi SOMO which took its time with issuing its May OSPs and only did so in mid-April. Arguably, by that point, it became evident that Chinese COVID-19 lockdowns will be a much bigger threat to regional demand in Asia than initially assumed and Baghdad took that into account by increasing its Asian OSPs by $2.30-$2.60 per barrel, almost half of what Saudi Aramco and NIOC did (even though the pricing basis, the Oman/Dubai average, is the same). In addition, the pricing moderation might have been impacted by India’s buying of Russian Urals. Given the geographic proximity and largely unmarred history of cooperation between the two countries, India has traditionally been a large buyer of Iraqi barrels and the sudden inflow of Russian will primarily hit Iraq. This would also be corroborated by Basrah Heavy witnessing the larger month-on-month increase, with Basrah Medium only hiked by $2.30 per barrel.

Chart 5. Iraqi Official Selling Prices for European cargoes (vs Brent Dated).

Whilst one might argue that SOMO’s Asian pricing for May replicates what Saudi Aramco did but instead keeps the increases moderate, the European prices of the Iraqi state oil marketer buck the Middle Eastern trend completely. SOMO cut the nominal May OSP of Kirkuk by 80 cents per barrel but that has very little immediate effect on the market as all the Kurdish barrels are still marketed by the regional government in Erbil. The pricing of Basrah Medium and Basrah Heavy, on the other hand, do matter and they saw their OSPs cut by $1.20 and $1.55 per barrel, respectively. Cognizant that Russian exports are squeezing its barrels out of traditional outlets, SOMO has seemingly decided to counteract the trend by pushing harder for its share of the pie in the Mediterranean (exports to NW Europe have routinely been meagre, averaging around 50,000 b/d). With Med buyers maintaining historically elevated levels of Urals buying, this will be quite difficult to pull off.

Chart 6. Iranian Official Selling Prices for Asia-bound cargoes (vs Oman/Dubai average).

Oddly enough, Iran’s national oil company decided to convey an even more aggressive pricing message to the markets and increased its Asia-bound May OSPs for Iran Light and Iran Heavy by 4.50 and 4.30 per barrel, respectively. Given that Iran still sells the overwhelming majority of its exports surreptitiously, at steep discounts to the officially declared formula prices, the price has little bearing on actual developments but is a strong signal to the market, a signal of a more confident Iran. Crude flows corroborate this as January-February loadings have averaged some 800-900,000 b/d, the highest since the ultimate wind-down of sanction waivers in May-June 2019. At the same time, as time goes by, the market’s faith in a viable Iranian deal continues to fade. With Teheran and Washington locked in mutual recriminations, Iranian negotiators and lawmakers have tried to reiterate the demands that have so far been unmet throughout the Vienna talks, mostly guarantees that the US does not repeat its deal departure and does not slap additional sanctions on Iranian entities.

Chart 7. Kuwaiti Official Selling Prices for Asian cargoes (vs Oman/Dubai average).

Of all main Middle Eastern producers, Kuwait has seen the most political volatility over the past weeks. The entire government led by Sheikh Sabah Khaled al-Hamad al-Sabah offered its resignation three months after taking office and surprisingly crude has been one of the key factors of destabilization. Despite maintaining objectives long-term goals, current production of the Kuwaiti national oil company KPC has been stagnating with the giant Burgan field marginally declining and new projects, such as joint production with Saudi Aramco in the Neutral Zone, failing to live up to the hype. Consequently, Kuwait has been searching for partners to help finance its spare capacity increases and Japan has reportedly agreed to provide $1 billion for that purpose. In terms of pricing, KPC hiked the May OSP of its flagship Kuwait Export Blend by $4.50 per barrel to a $9.30 per barrel premium vs Oman/Dubai, 10 cents higher than the Saudi m-o-m increase (bringing it to a total parity with Arab Medium).